Every great financial catastrophe in history has shared one defining feature: at the moment of maximum danger, the people most exposed were the most convinced they were safe. The railroad barons of the 1840s, the dot-com visionaries of the late 1990s, the mortgage engineers of 2007, all of them were, in their own minds, riding a permanent wave of transformative progress. They weren’t wrong about the technology. They were catastrophically wrong about the price they were paying for it.

We are living through that moment again. Right now. And the tragedy is that the very executives, fund managers, and policymakers who should be sounding the alarm are instead queuing up to pour more capital into the fire.

The Flattering Lie of “This Time Is Different”

AI is a genuine revolution. Let us state that plainly, so we cannot be dismissed as Luddites. The fifth industrial revolution, following steam, steel and electrification, mass computation, and internet connectivity, will reshape how value is created, how decisions are made, and how power is distributed. The productivity gains ahead are real. The economic transformation is not a fiction.

But here is the economist’s cold truth that no one in the room wants to hear: the reality of a technological revolution has never, not once in history, prevented the financial bubble around it from collapsing. The British railway network that transformed commerce in the 19th century was built on the wreckage of thousands of bankrupted investors. The fiber-optic cables that today carry the internet were laid during a frenzy that vaporized $5 trillion in equity value between 2000 and 2002. The infrastructure survived. The leverage did not.

“The technology was real. The valuation was a hallucination.”

What makes the current AI bubble distinctly more dangerous than its predecessors is not the scale of the enthusiasm, it is the nature of the collateral. When the dot-com boom collapsed, the fiber-optic cables that went into receivership didn’t disintegrate. They were purchased at cents on the dollar by new entrants and continued to function, carrying the internet traffic that eventually justified their existence. The physical assets retained economic utility even as the companies that built them went bankrupt.

AI data centers are being financed against Nvidia chips whose effective economic life is two to three years. The accounting models stretching depreciation to five or six years are not conservative estimates, they are a form of financial fiction that private credit markets are willingly, eagerly, accepting. When the next generation of hardware renders today’s GPU clusters obsolete, not metaphorically obsolete, but genuinely uncompetitive, the collateral securing hundreds of billions in leveraged loans will not be worth a fraction of the loans themselves.

Problem Masquerading as a Finance Problem

From a management consulting perspective, what we are observing across boardrooms is a catastrophic failure of competitive intelligence dressed up as bold strategic vision. Executives are not investing in AI because they have rigorously modeled the returns. They are investing because their competitors are investing, because their investors are demanding it, and because “AI strategy” has become the new prerequisite for a credible earnings call.

This is not strategy. It is mimicry with leverage attached.

The uncomfortable question that no management consultant currently billing $500,000 a month to an AI transformation program wants to ask their client is this: What is your actual payback period? Not the one in the slide deck. The real one, stress-tested against two-year chip obsolescence cycles, regulatory intervention, energy supply constraints, and a credit market that eventually reprices risk.

The Macro Threat No One Is Modeling

Zoom out to the global picture and the fragility compounds. The IMF is right to warn of recession risk, the Strait of Hormuz situation, sovereign bond pressures across the G7, and a looming food and energy price spiral are all genuine threats. But consider what happens when you overlay an AI equity correction onto an already-stressed global financial system.

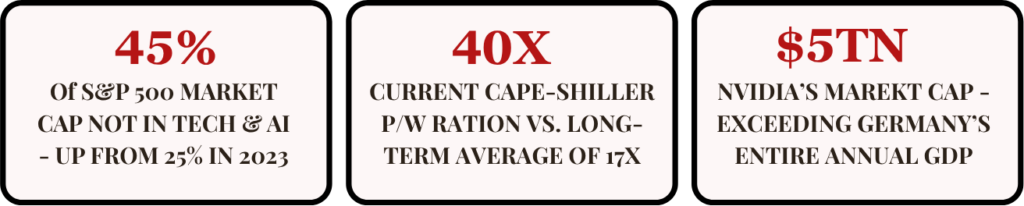

AI and tech stocks now represent 45% of the S&P 500’s market capitalization. A mean reversion to historical valuation norms would not be a correction. It would be an event. Pension funds, sovereign wealth funds, retail investors through passive index products – the exposure is systemic and largely unacknowledged. A Cape-Shiller ratio above 40 crashing toward its long-term average of 17 would destroy more household and institutional wealth than the 2008 financial crisis, in a global economy already running on empty fiscal reserves.

And unlike 2008, there is no obvious policy lever left to pull. Interest rates have limited room. Government balance sheets are stretched. The political appetite for further bailouts of financial institutions, or the tech industry, is somewhere between minimal and nonexistent.

“The exit is smaller than anyone thinks, and far more people are standing in front of it.”

What Serious Leaders Must Do – Now

This is not a call to abandon AI investment. It is a call to invest like adults. That means three things.

First, demand real payback models. Every AI capital expenditure should be stress-tested against a 24-month hardware obsolescence cycle, regulatory friction, and a credit environment where private leverage becomes unavailable. If the investment does not survive those conditions, it is not a strategic investment. It is a bet on conditions remaining perfect indefinitely.

Second, treat AI infrastructure debt as what it is. Organizations financing AI capability through leveraged instruments backed by depreciating hardware are not investing in the future. They are borrowing against an asset that will be worth significantly less before the loan matures. Boards have a fiduciary obligation to understand what is on their balance sheets, and what is being used to secure it.

Third, separate the technology from the valuation. AI will be transformative. Many of the companies currently valued as though they have already captured that transformation will not survive to see it. The ability to distinguish between the two, to invest in the durable capability without overpaying for the speculative premium, is the defining strategic skill of this moment.

History does not reward those who were right about the technology. It rewards those who were right about the price.

Analysis draws on publicly available market data, IMF economic forecasts, and Cape-Shiller index methodology. This article represents editorial opinion and does not constitute investment advice. All figures cited reflect conditions as of April 2026.