For years, the assumption held: no serious actor would weaponize a critical AI infrastructure chokepoint. The system was too interdependent. The costs of disruption would fall on everyone, including the disruptor. It was self-defeating by design.

And then someone was reckless enough to try it. And it worked.

The moment a dominant infrastructure provider demonstrated that controlling a single critical layer of the AI supply chain could generate leverage, extract rents, and command attention at the highest levels of commerce and government, the calculus changed, permanently. The playbook was proven. And proven playbooks get copied.Here is what the tech world is being forced to learn, slowly and expensively: AI infrastructure has chokepoints too. Compute. Frontier model access. Data pipelines. API dependency layers. Cloud substrate. Any one of them, controlled tightly enough, becomes a tollbooth. And once someone successfully runs a tollbooth, everyone with a strategically positioned narrow passage starts doing the math.

The Numbers Behind the Chokepoints

Real-world data on AI infrastructure concentration, cost exposure, and the sovereign AI program surge. Sources: Synergy Research Group, NVIDIA earnings reports, Stanford HAI AI Index 2024, OECD AI Policy Observatory, Goldman Sachs AI infrastructure research.

The Anatomy of an AI Chokepoint

Maritime strategists have long catalogued the world’s critical waterways, narrow passages where geography concentrates traffic, and where control translates directly into leverage. The AI stack has an equivalent map, and most organizations have never looked at it seriously.

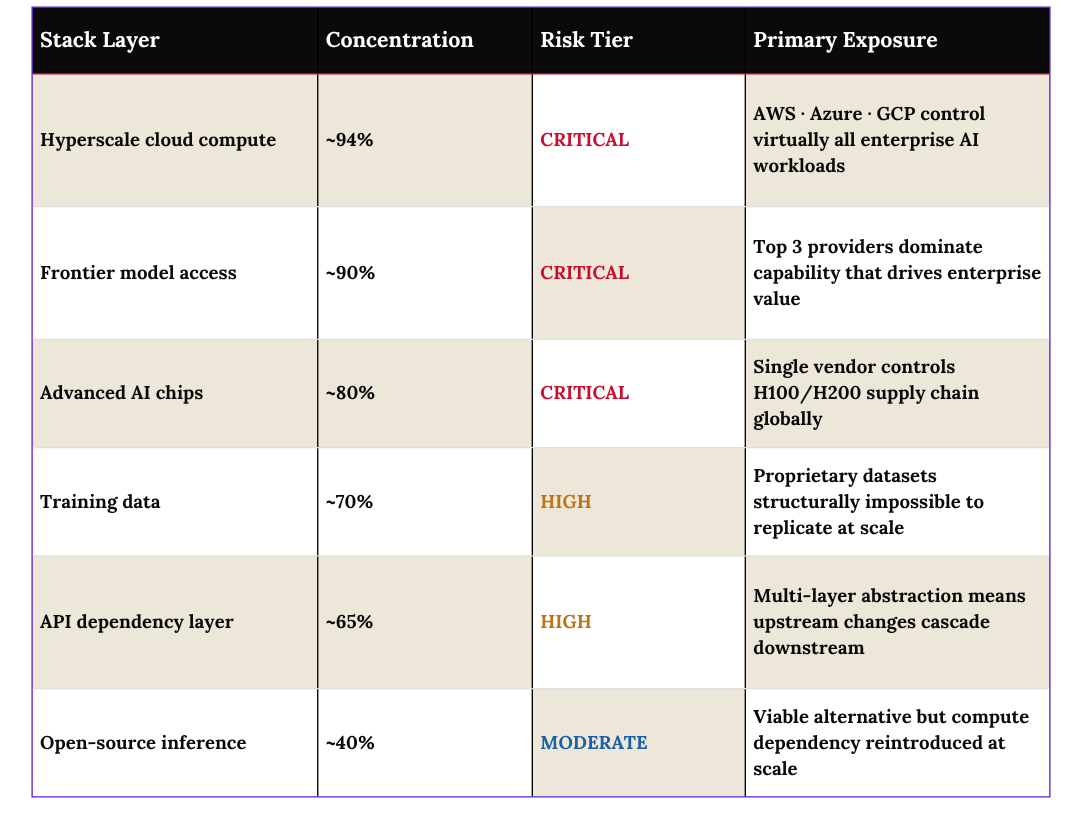

The critical chokepoints in today’s AI infrastructure include:

- Frontier model access. A handful of providers, concentrated to an extraordinary degree, control the capabilities that define what is commercially viable in enterprise AI. Switching costs are high. Alternatives exist but underperform where it matters most.

- Compute infrastructure. Advanced AI chips are physically scarce and geographically concentrated in their manufacture, their supply chain, and their data center deployment. This is not a software problem. It cannot be patched.

- Training data. The datasets that produce high-performance models are increasingly proprietary, legally contested, or structurally impossible to replicate at scale. First-mover accumulation has produced durable advantages that look increasingly permanent.

- API dependency layers. The average enterprise AI deployment is several abstraction layers deep. A pricing change, a policy shift, or a capacity restriction at any layer propagates downstream, often without warning.

- Cloud substrate. AI workloads are overwhelmingly concentrated in a small number of hyperscale cloud providers. Redundancy is assumed. It frequently does not exist in the form organizations believe it does.

None of these chokepoints is new. What is new is the demonstrated willingness to use them as leverage, and the speed with which that demonstration has changed behavior across the industry.

The Mimicry Problem

The most dangerous moment in any disruption is not the first incident. It is the normalization that follows.

Once the market accepts that a chokepoint can be monetized through leverage rather than efficiency, that value can be extracted not by building something better but by controlling something critical, the logic spreads with remarkable speed. Observers who were horrified by the original act begin calculating whether their own position affords similar options.

In the AI context, this mimicry is already visible in the architecture of sovereign AI programs. Governments that once framed domestic AI infrastructure in terms of capability development are now explicitly framing it in terms of leverage , the ability to restrict, condition, or tax access to capabilities that foreign enterprises need. What looked like protectionism begins to look like strategic positioning. The language shifts. The intent crystallizes.

Hardware export controls follow the same trajectory. What began as emergency national security measures have become permanent instruments of economic negotiation, applied, adjusted, and sometimes weaponized according to the geopolitical moment. The precedent is set. The tool exists. And the temptation to use it does not diminish.

What looked like a one-off disruption is becoming the new architecture of AI power.

The Stack Is More Fragile Than It Looks

Most enterprise leaders still think about AI access the way they thought about cloud computing in 2015, abundant, competitive, and essentially commodity. That mental model is dangerously out of date.

Concentration at the frontier model layer is extreme by any historical measure. A small number of providers control the capabilities that matter most for the use cases that are actually driving enterprise value. This is not a temporary condition of an immature market. It is a structural outcome of the economics of frontier AI development — the capital requirements, the data advantages, and the network effects of deployment scale all favor consolidation.

The “alternative routes” exist. Open-source models, regional providers, on-premise deployment, the options are real. But they carry significant limitations that most enterprise deployments have not stress-tested. Capability gaps are real and material. Integration costs are substantial. And the inference infrastructure required to run capable open-source models at enterprise scale reintroduces compute dependencies that organizations believed they were escaping.

The redundancy most organizations assume they have does not exist in the form they believe. This is the exposure that strategic adversaries, whether commercial or sovereign, are now actively assessing.

The Cost Signal Is Already Visible

When physical trade routes are disrupted, the cost signal is immediate and legible. Freight rates spike. Insurance premiums climb. The price of everything that moved through that route adjusts accordingly, visibly, quickly, and politically uncomfortably.

The AI equivalent is arriving more gradually, but it is arriving. Priority API access during periods of high demand. Reserved compute capacity for premium enterprise tiers. Model access conditioned on compliance with provider policy frameworks that can change without negotiation. The structural dynamic, where the chokepoint holder can impose costs on those who have no alternative, is already present in how leading providers are architecting their enterprise agreements.

This is not a complaint about provider behavior. Providers are making rational decisions. The point is that organizations which have built deep operational dependency on a small number of AI providers are now in a structurally exposed position, one they may not recognize as such until the cost of that exposure becomes undeniable.

By that point, the options narrow considerably.

The Genie Problem

The deepest problem is not any single provider’s behavior. It is that the precedent now exists.

Once it has been demonstrated that controlling an AI chokepoint generates real leverage against major players, including sovereign governments and the largest enterprises in the world — that strategy becomes available to every actor positioned to replicate it. The logic doesn’t require malicious intent. It requires only rational self-interest and a strategically narrow pipe.

Semiconductor control. Training data exclusivity. Inference infrastructure in a critical geography. Regulatory frameworks that condition market access on compliance with national AI standards. Each of these is a potential tollbooth. Each of them is being evaluated, right now, by actors with the positioning to use them.

And here is the parallel that should concern every board member and senior executive: even if the original disruptor ultimately steps back, even if the situation resolves in a way that restores nominal normalcy, the act has already set the precedent. The next actor considering a similar strategy doesn’t ask whether it has been done. They ask whether the conditions exist to do it again. And whether the other side has learned its lesson about dependency.

What Boards Should Be Asking Right Now

The strategic response is not panic, and it is not paralysis. It is the kind of structured, unsentimental audit that any serious organization would apply to any other critical supply chain dependency.

The questions boards and executive teams should be driving:

- Where are our AI infrastructure dependencies most concentrated, by provider, by geography, and by layer of the stack?

- What is the realistic cost and capability impact of switching any of those dependencies under duress, rather than on a planned timeline?

- Do our enterprise agreements contain protections against unilateral pricing changes, capacity restrictions, or policy-driven access limitations?

- How much of our operational continuity is now contingent on AI systems that depend on a single provider or compute region?

- Are we treating AI vendor risk the same way we treat other category-one supply chain risks, with systematic monitoring, scenario planning, and board-level visibility?

- What would a 30-day disruption to our primary AI provider access actually cost us, in revenue, in operations, in competitive position?

Most organizations cannot answer these questions confidently. That gap is the exposure.

The Strategic Imperative

The organizations that will navigate this period well are not those with the deepest AI capabilities. They are those with the most defensible AI architectures, built with deliberate redundancy, contractual protections, and a realistic understanding of where the pipes narrow.

This requires a different kind of strategic work than most AI programs have prioritized. The focus to date has been on capability, on identifying use cases, deploying models, and measuring productivity gains. That work matters. But it has produced architectures that assume the current period of open, competitive access will continue indefinitely.

The structural signals say that assumption is increasingly fragile. The chokepoints are being identified. The leverage is being calculated. The precedents are being set.

Leaders who are still waiting for the disruption to become obvious before they act are operating on maritime logic in an age of drones and tollbooths. The freight costs four times what they were before. The slots at auction. And the queue builds at both ends of a waterway that everyone assumed would stay open.

The genie is out of the bottle. The question now is whether your organization has a seat at the negotiating table — or is simply paying the tolls.

Headline Metrics

Table 1 – Chokepoint Concentration by Stack Layer

Estimated provider concentration at each layer of enterprise AI infrastructure. Risk tier: Critical >85% | High 65–85% | Moderate 40 – 65%.

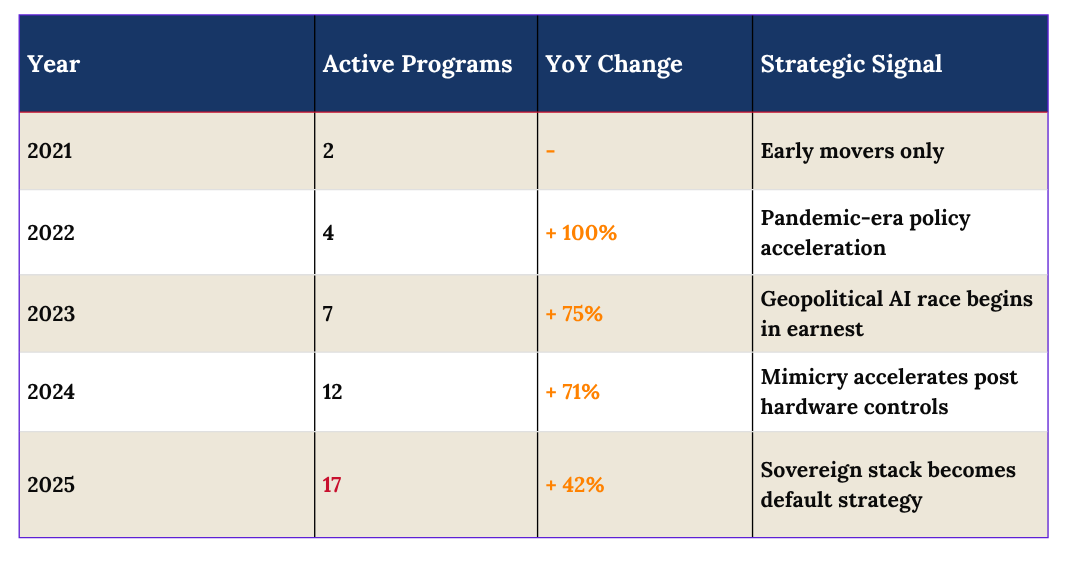

Table 2 – Sovereign AI Infrastructure Programs, G20 Economies

Number of G20 economies with active or formally announced sovereign AI compute or model programs. Source: OECD AI Policy Observatory.

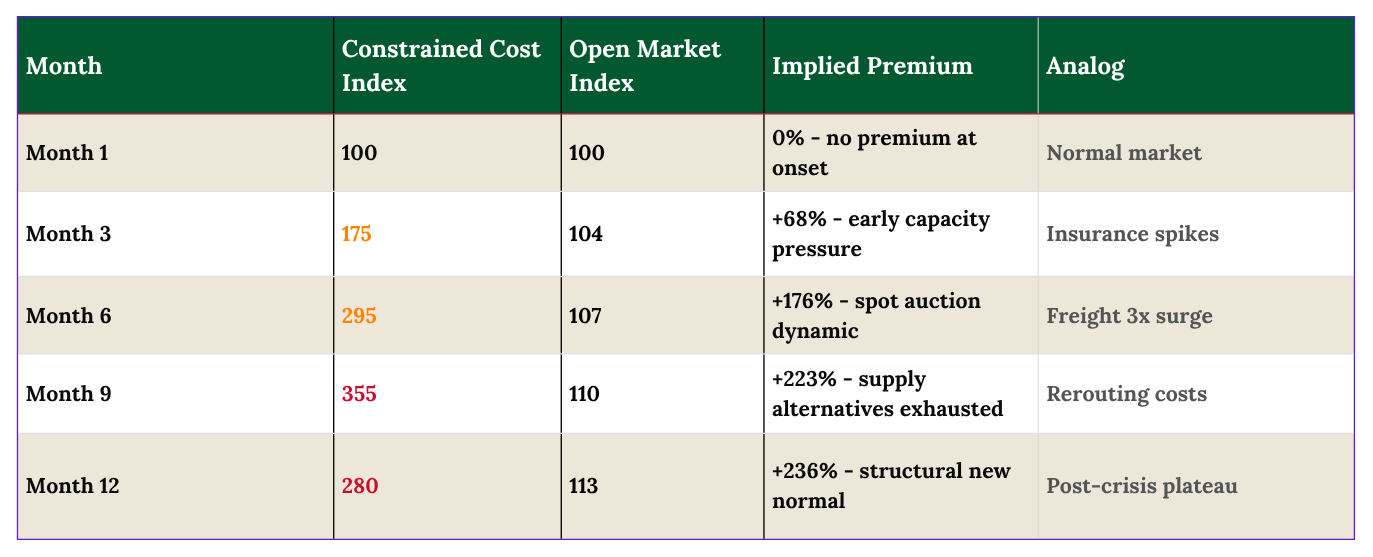

Table 3 – Cost Index Under Supply Constraint

Illustrative cost trajectory for AI compute and frontier model access during a supply constraint event. Baseline = 100 (pre-constraint). Modeled on documented behavior of comparable physical infrastructure disruptions (Red Sea routing, Black Sea insurance events).

The maritime world spent twenty-five years assuming the Strait of Hormuz would never close, because closing it would be irrational. It closed. The AI infrastructure stack has its own straits, narrower than most leaders realize, and watched by more actors than most boards have been told. The tolls are coming. The only question is whether your organization finds out at the negotiating table or at the invoice.

[© Copyright 2026. Norm Murray. All Rights Reserved.]